When it comes to debt collection, time is quite literally money. For businesses managing accounts receivable, understanding the statute of limitations on debt collection isn't just a legal technicality. It's a fundamental component of effective financial management.

Did you know that in 2023, U.S. businesses had more than $1.76 trillion in outstanding receivables, with approximately 18% of those accounts aging beyond 90 days?

Once an account ages beyond the statute of limitations, your options to collect become restricted, turning recoverable assets into write-offs.

As we examine the effects of debt collection statutes in all 50 states, let's see how grasping these time limits can reshape your strategy for managing accounts receivable and support a healthy cash flow for your business.

The statute of limitations represents a critical timeline that every creditor and financial professional needs to understand for effective debt recovery.

The statute of limitations for debt establishes the legal timeframe in which creditors can file a lawsuit against debtors for non-payment. After this period elapses, the debt is considered "time-barred," altering your options for recovery.

Quick Stat: Over 28% of Americans have at least one debt in collections on their credit report, many approaching statute expiration dates. (Consumer Financial Protection Bureau)

The statute of limitations limits legal remedies for debt collection, but does not eliminate the debt. If a debt exceeds this timeline, courts typically dismiss collection lawsuits when the debtor invokes the statute of limitations as a defense.

Understanding these variations demands attention to detail.

For example, credit card debt may have a 3-year collection window in Delaware and 6 years in Pennsylvania. It affects the collection strategy and resource allocation across states.

Even when a debt becomes time-barred, creditors maintain certain rights and options, though with significant restrictions:

Tip: Document all communication attempts with debtors, as certain actions by the debtor can potentially restart the statute of limitations clock in some jurisdictions.

Creditors face major risks under the Fair Debt Collection Practices Act (FDCPA) when collecting time-barred debts. Misrepresenting the ability to sue or threatening legal action on expired debts can lead to significant penalties.

Many businesses find that outsourcing professional debt management to companies like South District Group becomes increasingly necessary as accounts age toward their limitation periods.

Their state-specific strategies help businesses maximize recovery before accounts hit statutory limits, ensuring compliance with state and federal regulations.

Now, let's examine how different types of debt carry their unique limitation periods across various states.

Understanding how limitation periods vary by debt type is essential for an effective collection strategy, as each category follows different rules across jurisdictions.

Let's briefly understand them.

Open-ended accounts like credit cards and revolving lines of credit typically have limitation periods that begin from the date of last activity or default. These accounts remain open until formally closed by either party.

The ongoing nature of these accounts complicates determining when the limitation clock starts. In most states, it begins when the account is delinquent and no payments are made. However, in some jurisdictions, acknowledging the debt can restart the clock.

Written contracts provide the strongest documentation for debt collection purposes and generally receive longer statute of limitations periods than other debt types.

These agreements—such as auto loans, personal loans, and business financing contracts—are supported by clearly documented terms that courts can reference.

The limitation period usually starts on the date of the first default, which occurs when the debtor does not meet the payment terms outlined in the contract.

Most states allow 4-6 years for written contract collection, though some extend this period to 10 years, recognizing the definitive nature of written agreements.

Verbal agreements present unique challenges in debt collection, with generally shorter limitation periods reflecting their difficult-to-prove nature.

Oral contracts lack specific written terms and depend on witness accounts and payment records to prove their validity. This built-in uncertainty causes most states to impose a collection period limit of 2-4 years.

Collection professionals need to act swiftly on these accounts because the mix of insufficient documentation and tight deadlines renders them especially susceptible to being time-barred.

These formal written promises to repay specific amounts by certain dates often receive the longest statute of limitations periods.

Promissory notes merge written contract definitiveness with explicit debt acknowledgment, establishing a solid legal basis for collections. Their defined terms and schedules clarify default dates, ensuring certainty on the start of limitation periods.

Many states grant 6 to 10 years of windows for promissory note collection, recognizing their strong legal standing among debt instruments.

The variation in how states classify and limit different debt types creates a complex matrix for collection professionals to navigate.

For example, Florida maintains a 5-year limitation on written contracts but reduces this to 4 years for open accounts. Meanwhile, Kentucky applies 15 years to written contracts but only 5 years to open accounts.

South District Group maintains state-specific limitation period databases, aiding clients in prioritizing collection efforts based on remaining legal windows. This approach focuses resources on the accounts with the best recovery prospects.

Let's examine how specific states handle these limitation periods and what that means for your collection strategy.

Understanding how limitation periods vary across state lines is essential for crafting effective collection strategies that maximize recovery while ensuring legal compliance.

Let's have a look at the state-specific timelines for the Statute of Limitations.

The diverse legal landscape across America creates significant disparities in collection timeframes that can dramatically impact recovery outcomes.

Quick Stat: The difference between the shortest state statute - North Carolina, at 3 years for open accounts, and the longest - Kentucky, at 15 years for written contracts, represents a 400% variation in available collection time.

Consider these contrasting approaches:

These variations fundamentally impact the collection strategy. A debt portfolio that might be largely time-barred in California could remain fully collectible in states with longer limitation periods.

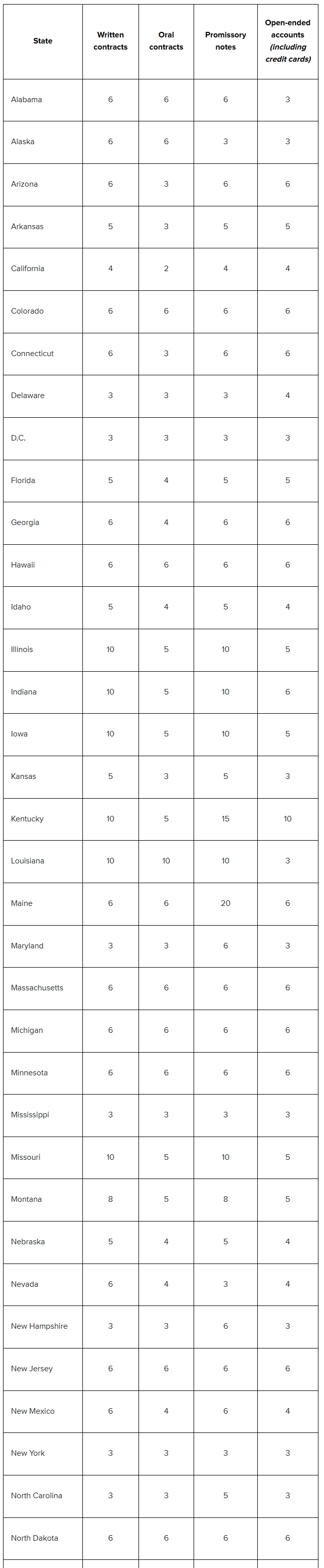

The following chart provides a snapshot of limitation periods across debt types for all fifty states:

Note: This table offers general information and is not legal advice. Statutes may change, affecting the limitation period. Always consult a qualified legal professional for specific guidance.

When acquiring debt portfolios that span multiple states, prioritize collection efforts based on remaining legal windows, focusing first on states with shorter limitation periods.

Geographic variation presents challenges and opportunities. Multi-state operations need advanced tracking for limitation periods per account.

Understanding these differences allows strategic resource allocation, directing collection efforts where legal recourse is strongest.

South District Group's nationwide network of legal representatives allows for optimized collection strategies that account for state-specific limitations.

By utilizing local expertise in each jurisdiction, SDG helps clients navigate these varying timeframes, ensuring appropriate action before statutory deadlines expire.

Having examined these state-specific timelines, let's explore how specific events and circumstances can affect the statute of limitations for your receivables.

Effective debt collection involves understanding not just the timeframes but also how various factors can affect the statute of limitations across jurisdictions.

Here are some strategies that you can implement to streamline your debt collection policies.

When debtors relocate across state lines, the question of which state's statute applies becomes immediately relevant to your collection strategy.

Most courts use the "most significant relationship" test, evaluating the debt's origin, payment locations, and parties' residences to determine which state's laws govern the limitation period.

For example, if a debt originated in Texas but the debtor now lives in Florida, Texas's 4-year limitation might apply rather than Florida's 5-year period.

This mobility complicates tracking limitation periods. When debtors move, collectors must assess if the original state's statute applies or if the new state's rules take precedence, often necessitating legal analysis for each account.

The statute of limitations typically begins on the date of first default, when the debtor first misses a required payment without bringing the account current.

What makes this particularly challenging is that certain debtor actions can restart the limitation clock in many states.

These include:

For example, if a debtor makes even a $10 payment on a $5,000 debt that's nearly time-barred, this could potentially reset the entire limitation period in states like Florida, giving collectors several more years to pursue legal action.

When a debt exceeds its statute of limitations, collection options narrow but don't disappear entirely.

Creditors can request payment through non-litigation means but must avoid threats of legal action or misrepresentation. Some states require disclosures when collecting time-barred debts, informing debtors that the debt cannot be legally enforced in court.

Settlement negotiations can still be effective after they expire, since many consumers wish to settle past debts to enhance their credit scores or to gain peace of mind. These negotiations typically focus on significant reductions from the original balance.

At South District Group, our compliance-focused collection strategies account for these state-specific variations regarding limitation periods. Our account management system tracks reset events and applies collection approaches based on legal status, ensuring recovery without violating compliance.

Now let's examine how time-barred debt affects legal proceedings and what options remain available when limitation periods expire.

When a debt exceeds its statute of limitations, it becomes "time-barred," creating significant implications for both creditors and debtors. While legal collection options become limited, these debts can still affect your financial life in various ways.

Time-barred debt is debt that has surpassed the statute of limitations for legal collection. It doesn't mean the debt disappears or is forgiven; it restricts the creditor's ability to sue for recovery.

Quick Stat: Approximately 1 in 4 consumers contacted about a debt report being pursued for debts they don't believe they owe, which often includes time-barred debts. Consumer Financial Protection Bureau

When a debt becomes time-barred, creditors and collection agencies may still:

However, they cannot legally threaten to sue you or take you to court over this debt. Doing so would violate the Fair Debt Collection Practices Act (FDCPA).

Despite legal restrictions, some collectors may still file lawsuits, hoping that debtors will not recognize the debt is time-barred or will fail to appear in court.

Tip: Never ignore a summons, even if you believe the debt is time-barred. Failing to respond typically results in a default judgment against you, which can lead to wage garnishment or bank account levies.

If you're sued for a time-barred debt, you have several potential responses:

Keep in mind that the statute of limitations is an affirmative defense that you need to assert on your own. The court will not dismiss a case solely because the debt is time-barred unless you bring this to their attention.

If a creditor successfully obtains a judgment before the statute of limitations expires, this creates a new legal obligation with its own (typically longer) enforcement period.

Judgment enforcement periods typically range from 5 to 20 years, with many states allowing judgments to be renewed for additional periods.

Once a judgment is obtained, creditors gain powerful collection tools that may include:

These judgment enforcement tools remain available even if the original debt would have become time-barred during the judgment enforcement period, and thus, a proper response to any lawsuit is critical to preventing a judgment.

South District Group understands the interplay between statutes of limitation and debt recovery. Our team evaluates accounts throughout their lifecycle, ensuring collection efforts comply with applicable laws while maximizing recovery for clients.

By thoroughly analyzing each account's legal status, we develop strategies that respect statutory limitations while providing ethical paths to resolution.

Now that you understand how time-barred debt affects legal actions, let's examine how these limitations interact with credit reporting and debt validation processes.

While the statute of limitations affects your legal liability for a debt, it operates independently from credit reporting timeframes and validation requirements.

Understanding these distinctions helps you manage your financial reputation even when dealing with older accounts.

The statute of limitations on debt collection and credit reporting periods are separate legal frameworks that operate independently of each other.

Most negative information, including late payments and collections, can legally remain on your credit report for 7 years, regardless of the statute of limitations in your state.

It creates several important scenarios to understand:

The impact is significant—even if a creditor can't sue you for a debt, it can still affect your credit score and ability to obtain loans, housing, or employment within the 7-year reporting period.

Tip: Before making any payment on an old debt, consider whether it's more beneficial to negotiate a "pay for delete" arrangement where the creditor agrees to remove the negative item entirely rather than updating it as "paid collection."

All consumers have the right to request validation of a debt under the Fair Debt Collection Practices Act (FDCPA), regardless of whether the debt is time-barred.

When you receive communication from a debt collector, you have 30 days to request debt validation.

It requires the collector to provide:

This validation process is crucial for older debts sold multiple times between collection agencies. Errors in documentation, incorrect amounts, and attempts to collect satisfied debts increase as accounts age.

If a collector cannot validate a debt upon request, they must cease collection activities. This protects against incorrect information on your credit report and collection attempts for debts you don't owe.

At South District Group, we maintain rigorous documentation and validation processes for all accounts in our portfolio.

Our account management methodology effectively validates all serviced debts, offering transparent information to consumers and safeguarding clients from compliance risks linked to improper validation.

Now that you understand how credit reporting and debt validation interact with statutes of limitation, let's explore some final thoughts on managing debt collection effectively.

Navigating debt collection statutes of limitation requires a thorough understanding of state-specific regulations and your rights under federal law.

These timeframes vary significantly across states and debt types, creating a complex landscape for both creditors and consumers. While time-barred debt may limit legal collection options, it doesn't eliminate all avenues for resolution.

Key Takeaways:

For creditors, knowing these limitations helps develop appropriate collection strategies that remain within legal boundaries.

South District Group brings over a decade of experience navigating these complex regulations across all fifty states. Our team merges legal expertise with analytics to create tailored liquidation strategies that honor statutory limitations and consumer rights.

Ready to transform your approach to debt recovery while maintaining compliance?

Contact South District Group today to discover how our nationwide network of legal representatives can help maximize your receiva